Everything you ever wanted to know about becoming a homeowner

Buying your first home is a big investment. We’re here to make the process as easy as possible and keep you informed every step of the way. Whether you’re a first-time homebuyer, are buying a luxury home, or are investing in properties to build your real estate portfolio, we can help guide you through the process toward getting that new set of keys!

Steps For Buying A Home

Congratulations! You’ve decided to buy a home. Before beginning the loan process, it’s important to do your research. There are many steps involved to make sure you have a smooth and successful experience. Start by getting pre-qualified. Simply fill out the pre-qualification form online and a licensed loan officer will contact you within 24 hours.

Pre-Qualify

What is pre-qualification?

Pre-qualification determines your ability to repay a loan based on information you provide. Your liability, asset and income information are reviewed by a licensed mortgage loan originator to establish the maximum purchase price you can afford and how much you may be able to borrow.

What are the benefits of pre-qualifying today?

Pre-qualification may establish you as a serious buyer when looking at real estate, give you an advantage over other buyers looking at the same property, and let you know what you can afford before home shopping.

Understanding Your Credit Report

Your credit score is not the only factor in getting approved for a mortgage, but it is an important part of determining what you will be able to qualify for.

- Check your own credit score before meeting with a lender.

It’s important to make sure that your score is accurate when applying for a loan. You can get a free credit report once a year online by visiting annualcreditreport.com. - Verify report for accurate information.

Report and dispute inaccuracies with the credit bureau. Disputes in process may delay loan approval. - Paying down high credit balances may positively affect your credit score.

By paying down applicable lines of credit before applying for a loan, you may qualify and get approved for a better interest rate. - Set up payment plans.

Call your creditors and work out a budget-friendly payment plan on delinquent accounts prior to applying for a loan. Work out a plan that won’t harshly affect your debt-to-income ratio but will still let lenders know you are serious about being credible for your debts.

Meet Your Licensed Loan Originator

If you pre-qualified, you should be in contact with a licensed loan originator. If you have not, give us a call today to discuss your options and get started. Together, we’ll choose a mortgage product that will meet your needs. If you want to get an idea of what kind of product may be right for you, see our loan types. A licensed loan originator will assess your financial situation and make a recommendation.

Estimate Your Expenses

Use our online calculators to get a general idea of how much home you can afford. Determine how much home you can afford, what your estimated monthly mortgage payment may be, how much your down payment should be, and more. When budgeting to plan for a mortgage, a loan originator will help you include:

- monthly bills

- estimated property taxes

- estimated home-owner’s insurance

- estimated private mortgage insurance (PMI)

- living costs

- potential Home Owners Association fees

In addition to ongoing costs, remember to factor in one-time costs during the buying process, including closing costs and your down payment.

Get Pre-Approved

Pre-Qualification

It determines your ability to repay a loan based on information you provide. Your liability, asset and income information are reviewed by a licensed mortgage loan originator to establish the maximum purchase price you can afford and how much you may be able to borrow.

Pre-Approval

This is a written commitment from a lender to extend a mortgage to you for a specific amount and time period.

It is important to understand the difference between pre-qualification and pre-approval. A Pre-qualification determines your ability to repay a loan based on information you provide. Your liability, asset and income information are reviewed by a licensed mortgage loan originator to establish the maximum purchase price you can afford and how much you may be able to borrow. A Pre-approval is when your information is reviewed and verified by an underwriter. This involves an analysis of your financial status and credit history. With a pre-approval, you’ll be able to negotiate your home purchase confidently. Realtors and sellers will often take your offer more seriously if you get pre-approved prior to house shopping because it lets them know you are ready to make a deal. A pre-approval may help streamline your process and result in a smoother transaction.

Find The Right Realtor

Now that you have initiated the pre-approval process, and have an idea of how much you are comfortable spending, a realtor can help you through the home buying process. Finding the right realtor is just as important as finding the right lender. Make sure that you work with a real estate agent you can trust, has a proven track record, and has your best interests at heart. It’s useful to get referrals from family and friends who’ve been through the home buying process.

Avoid Dual Agents.

It is also commonly advised to avoid dual agents when going through the home buying process. A dual agent is a real estate agent who represents both the buyer and seller in a transaction. This is often a conflict of interest since it’s possible that the agent will not negotiate in the buyer’s interest in order to increase the commission. If you do use a dual agent, make sure it’s someone you trust completely.

Interview several agents before choosing one.

You may consider asking them a set of similar questions:

- How long have you worked in real estate?

- Is this your full-time job?

- Have you sold homes in the area I am interested in before?

- How many sales in this area have you done?

- How many sales have you done in the last year?

- Will you be present for the closing of my loan?

Start House Hunting

You have a lender and you have a realtor. Your next step will be to start looking at houses. It is easy to get carried away with the excitement of becoming a homeowner at this point. You may only be thinking about yard space, decorations and the amount of bedrooms you want, but it is important to consider all aspects of the property before moving forward.

Location is key!

Consider the crime rate, public school ratings, your daily commute, traffic patterns, and local amenities when choosing a home. If public parks, libraries, pools, sporting arenas, churches, restaurants or shopping centers are important to you, make sure you consider their proximity to your neighborhood before getting lost in visions of porch swings and curtains.

Be aware of the condition the home is in.

You may think you have found your dream home, but keep in mind any extra stress or costs that may come up when you’re learning about that crack in the wall or the furnace system from decades ago. If you’re going for a fixer-upper, make sure you have factored in time to your moving process, in addition to additional expenses. (Also note that an FHA203(k) will allow a buyer to finance qualified repairs).

Start The Loan Process

By now, you’ve obtained your lender, you’ve gotten pre-approved, and you’ve found your dream home. It is time to start the loan process! Meet with your licensed loan originator to help you gather paperwork and submit your mortgage application.

Gather all necessary identification and paperwork

Identity & Income Information

- Your full legal name, Social Security number, and date of birth. A copy of your Social Security card may be required.

- Your phone number, email address, and residential mailing addresses for the past two years.

- Your primary and secondary income and sources.

Your government-issued photo ID. - All employer names, addresses, and phone numbers for the past two years.

- The values of your bank, investment, and retirement accounts, as well as any other asset accounts.

- Your monthly debt obligations.

- The address of the property being purchased, year built, estimated down payment amount, and purchase price.

- Estimates of annual property taxes, homeowners insurance, and homeowner association dues (if any).

Income Information for Self-Employed Borrowers

- Your personal and business federal tax returns for the past three years.

- A year-to-date profit and loss statement.

- A complete list of all business debts.

Credit Information

- A letter of explanation for any late payments, judgments, collections, or other derogatory credit history items.

- Source of funds documentation for any large deposits on asset or bank statements.

- The judicial decree or court order of each obligation due to legal action.

- Bankruptcy/discharge papers for all bankruptcies in your credit history.

- Payment histories for utilities, cable TV, internet, phone, auto insurance, and any other expenses.

Income & Tax Documentation

- IRS Form 4506-T — request for tax transcript; must be completed, signed, and dated.

- Your W-2s for the past two years.

- Pay stubs for the past 30 days.

- Your federal tax returns (1040s) for the past two years.

- Your most recent two months’ asset and bank statements for all accounts on your application (all pages, including blank pages).

- A written explanation if you have been employed less than two years or if employment gaps exist.

- A purchase contract signed by all parties.

- Homeowners insurance information, including the agent’s name and phone number.

These documents may not be all-inclusive, but by having these on hand, you will expedite the application.

Submit your application

Fill out and sign Form 1003 — the residential loan application — including the attached fair lending notice, loan info sheet, and credit authorization. Note: Do not use whiteout on this paperwork. Mistakes should be crossed out and initialed.

Review your Loan Estimate

This document contains important details about the loan your are applying for including estimations of your interest rate, monthly payment, closing costs, taxes, insurance and any prepayment penalties. The lender must provide this to you within three business days of receiving your application.

Review your Good Faith Estimate

This is the list of the settlement charges that you must pay at closing. The lender must provide this to you within three business days of receiving the mortgage application.

Clear any additional requests from underwriting

Underwriting is the department that reviews all of your identification, paperwork, and credit history to asses if you will qualify for the desired loan. They determine the terms of the loan and will occasionally require extra documents to fully understand your background and make their decision. It is important to make yourself available during the underwriting process and to respond to any requests promptly and thoroughly.

Review your Closing Disclosure

The lender must provide this to you at least three business days before you close your loan. This document contains the final terms of your loan. Use this time frame to review it thoroughly and compare it to your loan estimate. Don’t be afraid to ask your lender questions if you are unclear about the terms.

Make Your Offer

You may want to keep several factors in mind as you and your real estate agent get ready to present an offer to the seller.

- The asking price of the home

- Recent home sales in the area

- Market conditions

- Prospective re-sale value

- Satisfaction with the neighborhood and amenities

- Condition of the home

- How many other prospective buyers are looking at this home

- If you have a back-up home in mind

After the offer is accepted

Before closing, clarify when the seller will be vacating the home. If they remain on the property after the closing date, you are entitled to negotiate rent payments.

Get A Home Appraisal

Inspections are important to help you fully understand the condition of a home. They can also be helpful for negotiations to help drive prices down or have additional services stipulated in the contract.

Take the time to get commitments in writing.

During the sales process, a seller may make a variety of verbal guarantees. For example, the seller may promise to fix the roof before move-in or provide all of the kitchen appliances. Make sure this information is included in writing in any agreements you sign. If an agreement is not explicitly written in a contract, the seller is not obligated to abide by it. This also includes all of the details of your loan. Make sure the amount, payments, rate lock, and other details are clearly stated in writing in a signed document.

Set Closing Date, Time and Location

Bring along any co-applicants and your realtor, if you would feel more comfortable having them present. Closing usually takes place in the presence of a public notary. You should be prepared for several things:

- Review the final documents. Make sure the rates and amounts are what you have agreed to.

- Bring a cashier’s check to cover the closing costs and down payment. Personal checks are usually not accepted.

- Sign the loan and be prepared to show photo ID and possibly a Social Security card.

If you currently have an apartment, condo or house lease

Consider scheduling your closing date around the time that your lease will be up. Some home-buyers prefer to not have a payment overlap, while others enjoy the overlap if they have projects that need to be completed in the new home.

Receive Your New Set of Keys

Congratulations, you are now a homeowner! Although you may now have the key to your future, don’t forget about the key to your mortgage. Scion Lending is here to offer you guidance on any future questions or situations that may arise. A licensed loan officer will always be available to help you refinance, use your home equity, or even purchase additional properties to build your investment portfolio.

Guides and Resources

Now that you understand the process that will take place, take the time to understand other benefits and aspects of buying a home. Check out these helpful links to learn more about the resources available to help guide you throughout the loan process.

These resources are available to help guide you throughout the loan process.

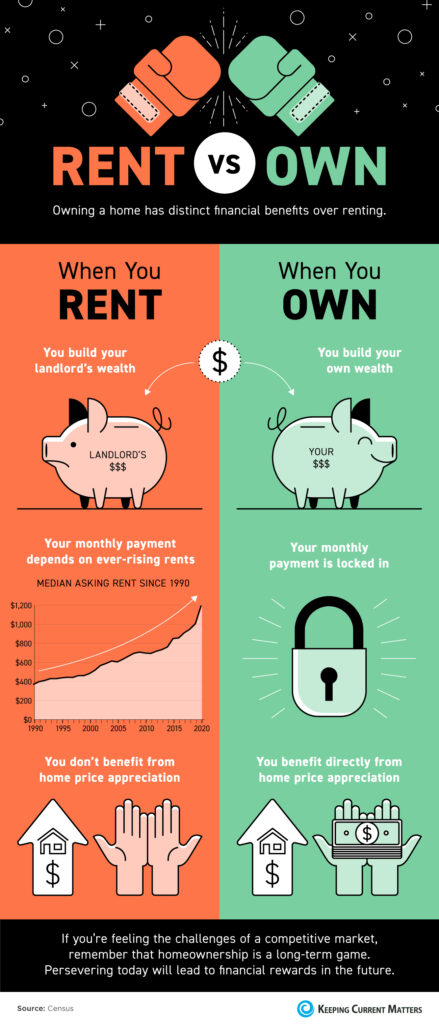

- Buy a Home – Learn about the benefits of owning your own home, as opposed to renting.

- Mortgage Glossary – Learn common mortgage terms that will be relevant to your home buying experience.

- Home Purchase FAQs – Consider the most frequently asked questions that our clients ask when buying a home.

- Tips for First-Time Homebuyers – Check out this special set of tips if you are a first-time home buyer.

- Understanding Down Payments – Not all down payments are created equal. Check out the various down payment requirements.

- Tax Advantages – Although you should speak with your professional tax adviser, often there are tax advantages when you purchase a home.

Are You Ready To Buy A Home?

If you think that you are ready to buy a home, then this is the right place for you. Below are general statements to help direct you to a purchase product that might be right for you. Simply complete the statement with an option that best fits what you’re looking for.

I Want To Buy A Home and I. . .

- Want stability in payments & rate

If you’re looking to budget for a loan payment that won’t change as market rates change, then a fixed-rate mortgage might be for you. You’ll have the security of knowing what your payment will be throughout the life of the loan.

Learn more - Want a low interest rate and am predicting that the rates will stay low while I own my property

If you’re looking for a rate that may be initially lower than a fixed-rate mortgage or don’t plan on living in your home long-term, then an adjustable-rate mortgage might be right for you.

Learn more - Want a property that needs renovations/improvements

If your dream home is a fixer-upper or one that needs improvements, then a FHA 203(k) may fit your need to combine a home loan and qualified improvement costs together into one payment.

Learn more - Want a luxury/high-priced property

More expensive or luxury dream homes often require loans that exceed the limit of a conventional home loan. A Scion Lending jumbo mortgage can provide up to $3 million in financing to help you secure your home purchase.

Learn more - Am a veteran

If you’re a veteran, then a VA home loan insured by the U.S. Department of Veteran Affairs can help provide favorable terms on your home loan. You don’t need to be a first-time home buyer and you can reuse the benefit.

Learn more - Am looking for a low down payment

Finding a home loan with a low down payment requirement, as low as 3.5%, is made possible through an FHA home loan, which is insured by the Federal Housing Administration. FHA loans can benefit first-time home-buyers who may need a co-signer on the loan or have less than perfect credit.

Learn more - Want a home in a rural area location

Through a USDA rural home loan, purchasing a home in a designated rural area can provide the benefits of flexible credit and low down payment requirements and the security of a fixed rate.

Learn more

Related Information

When you purchase a house, you want the best experts by your side. Find out about the benefits...

Our home purchase programs are designed to help any kind of borrower. Learn more about the...

Is it your first time buying a home? Check out our tips and advice for first-time homebuyer...